Car Buying Best Practices

22 February 2012

This is a collection of best practices for buying a car, compiled from several dozen Internet sources.

Process

- Write down what features you must have, want to have, and don’t care about.

- Do Internet research on which cars fit the bill.

- Eliminate all cars that don’t have your list of must-have features.

- If there are more than 8-10 cars remaining, eliminate the ones that barely fit your list.

- Test drive the remaining cars. Take notes about what you like and don’t like. Remove any cars you don’t like.

- Collect information about specific cars. Find the top deals.

- Call car dealers and sales folks, make them bid for your business

- Test drive the specific car you like. Inspect it carefully. Have a professional mechanic to inspect it for problems.

- Buy the car.

- Celebrate!

When test driving a car, check on:

- Acceleration from a stop

- Engine sound when cold

- Engine noise

- Does the car drift left or right when driving straight?

- Hill-climbing power

- Braking

- Cornering

- Turning radius

- Suspension

- Rattles / squeaks

Before Arriving:

- Agree to the price on the phone, before arriving

- Run a history check on the car

- Ask salesperson to email all of the taxes, fees, and price first

- Call your state DMV and ask about liens against the vehicle

Car Inspection

- Ask about the warranty

- Ask about return policy

- How worn is the brake pedal? Too much, and it’s shady

- Check outer edge of driver’s seat for wear

- Go under the floor mats. Check for water damage (leaks)

- Check the outer edges of the tires. If they’re worn, the front end is out of alignment

- Check for paint on the moldings/lights. Sign the car has been re-painted

- Check the engine. Is anything dirty, rusty, or worn?

Negotiating

- Always be ready to walk out

- Don’t get attached to any car

- Dealerships - end of the month is better

- Don’t sign up for add-ons

- If you don’t get it in writing, it does not exist.

- With a finance-and-insurance person, don’t get upsold. That’s their job, after all.

- Read the contract carefully

- Make sure you get a clean title

- Ask about return policy, get it in writing.

- Do not sign an ‘as is’ paper. Anything that says that needs to be removed

- Ask for the car’s maintenance record.

- Only go for normal fees

- License fees (title, registration, price set by each state)

- Documentation fee

- Smog (price set by each state)

- Sales tax

- Based on average fair market value of the car

- Not the purchase price

- Comes from Price Digests

- Rate is .65% from the state, .30% from King County

- Clark County is .12%, for a total of 0.77%

- Fees to question/call BS

- Dealer fees

- Dealer Prep

- Shipping

- Advertising fee

- “Internet” fee

- Window VIN etching

Considerations:

- Still under factory warranty?

- Does warranty transfer to new owner?

Tactics:

- Use Carfax to find a vehicle’s history

- Consider ‘program cars’

- Consider cars from rental companies

- Know the true market value (not Kelly Blue Book)

- Take it to a trusted mechanic to have them evaluate it

- http://static.ed.edmunds-media.com/unversioned/img/car-buying/used-car-worksheet/used.car.questionairre.pdf

- http://www.edmunds.com/car-buying/10-steps-to-buying-a-used-car-pg11.html

Buy a Car With Data - Part 2

14 February 2012

In our previous blog post we identified 27 cars based on a list of features, and then narrowed our list down to 3 based on Internet data and test drives. Now, it is time for more data!

Deep Dive

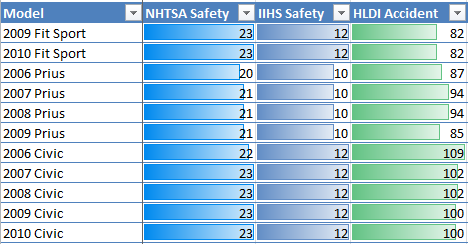

With a list of cars this small, we can do more in-depth research. We found out the cost of car insurance, average maintenance costs, vehicle crash ratings, accident data, and insurance data. We also tried to estimate how much each model would cost to own over 5 and 10 years.

However, the most interesting data was about crash test ratings and accident statistics. Vehicle crash-test ratings are designed to be predictive, which means they try to imitate real-world conditions. Accident data is far more interesting, because it shows what actually happened.

The Honda Civic accident data suggests it is less safe than a Fit or Prius. We eliminated it from our list. You can’t argue with data.

We are left with 2 options: the Prius and the Fit. It is time to look at specific cars for sale.

Round 3: Specific Cars

The Internet makes it easy to find data. In our case, we used AutoTrader.com and ToyotaCertified.com to get a list of cars within 200 miles of Seattle. We wanted to find any Prius or Fit for less than $20,000 and with under 60K miles. We found 105 cars. Now that we had data, it was time for analysis!

Analysis

Our biggest question was how to consider several variables. Which is better: a $15,000 car with 32,000 miles or a $12,000 car with 46,000 miles? What if one is a year older than the other?

The way we handled this is by focusing on the variables that mattered the most to us: price, mileage, and age. We created a ‘score’ for each car’s variable, from 0% to 100%. 100% meant it was the best deal. 0 mean it was the worst. For example, the car with the lowest mileage had a ‘mileage score’ of 100%.

To find a ‘Good Deal Score’, we weighted the different scores, and then added them. We said that price matters 50%, mileage 16.6%, age 16.6%, and warranties 16.6%.

You can see the results below. The best cars had a good deal score of over 5. You can see how the best scores are often given to cars with low mileage and a low price.

We looked at the top 2 Priuses and Fits, sorting by their Good Deal Score. We realized that the 2009 Prius for $15,000 and with 25,000 miles was what we wanted. We called the car dealer, had them email us the final price ($16.5K with sales tax and registration), and we bought the car that day. No pressure, no hassle, and we knew we got a great deal. Success!

Epilogue

Lessons Learned:

- The Internet levels the playing field. A few days’ research can make you a much savvier car shopper, giving car salesmen less of an edge.

- Remember that the buyer has all of the leverage. I can choose not to buy a car from someone at any time.

- Make car dealers bid for your business. Use phone or email, so they can’t pressure you.

Pros:

- Discussing features first was a brilliant idea. We both compromised to make that list of features, but in a low pressure situation. Later on, Kate & I never disagreed about whether a car was a good fit for us, because we both were looking for the same thing.

- Decide which model(s) to buy before deciding which specific car to buy.

- The amount of money you can save by comparison shopping is incredible. We could immediately tell whether a specific car was a good deal or not based on the data.

- A modest amount of time = massive savings. We spent ~40 hours doing research, analysis, and test drives That may save us $5,000 to $15,000 over the life of the car. That comes out to $125 to $375 saved per hour.

- Using data = fewer disagreements. Kate & I always agreed which car was safer, because the data told us. We knew which specific car was a better deal, because our analysis said so.

Limitations:

- Self awareness. Why are certain features and options important to you?

- Emotional control. It is hard to walk away from a nice car because you are not intellectually ready to buy it.

- Takes time. Those 40 hours were not spent on sleep, reading, or blogging.

What We Wish We Had:

- Car maintenance/reliability data. We still don’t know which car models are more reliable than others.

- Car price predictor data. We didn’t know whether car prices were going up or down.

- A service to do this for us. I would gladly pay $100 for some company to do all of this work, and deliver the car to my front door.